Insights from the Advice Map of Britain

A growing number of people across the UK find themselves in an ‘advice gap,’ missing out on the significant benefits that expert financial guidance can offer.

This situation begs the question: how can advisers broaden access to advice and help more people enjoy its benefits, while maintaining or even increasing success and profit?

Mapping Britain’s relationship with financial advice

To gain a deeper understanding of the individuals who fall within the advice gap and identify the steps needed to close it, we have created an “Advice Map of Britain”. As a dominant player in adviser practice management systems, with a market share of 52% according to NextWealth[i], we were able to review data from three million advised clients to uncover who is taking advice – and more importantly, who isn’t.

Our analysis revealed persistent disparities in access to financial advice. Key factors impacting an individual’s likelihood to seek advice include gender, age, relationship status, and geographic location.

Gender imbalance

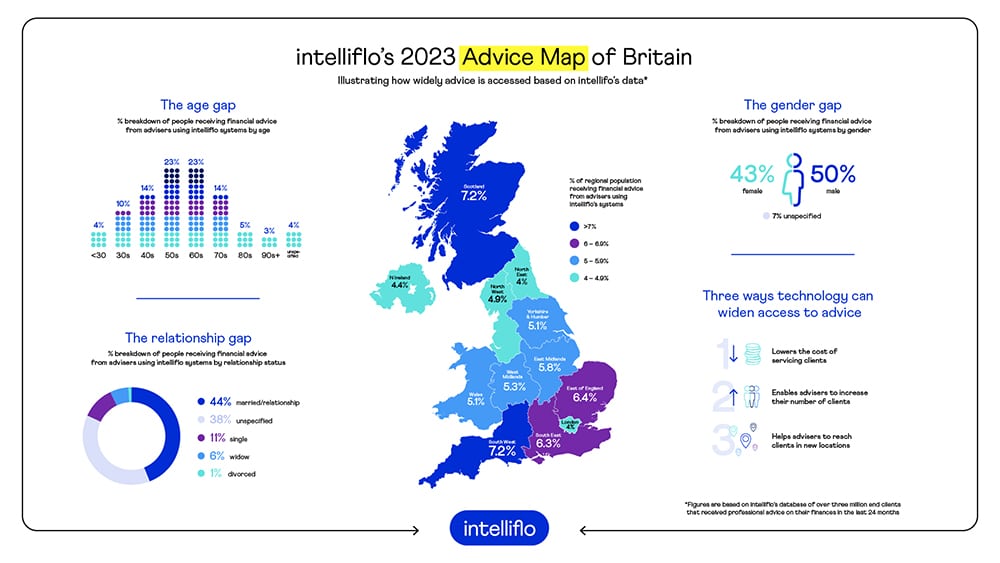

Being a man makes it more likely that you’ll seek financial advice. According to our data, half of advised clients are male and just over two-fifths (43%) are female (the gender of the remaining 7% is not specified). Northern Ireland has the widest gender advice gap, with 43% to 54% female to male, while London boasts the narrowest gap at 47% female and 50% male.

HMRC ISA subscription figures show that women are more likely to save than invest. In 2019/20 81% of women chose a cash ISA, 15% stocks and shares ISA and 4% both, compared to 71%, 22% and 6% of men respectively[ii]. By investing less, many women have less opportunity to grow their money, compounding wealth inequalities. Bringing more women into advice is crucial to their long-term financial security.

Generational disparity

Alongside the gender imbalance, our Advice Map also uncovers a significant age bias, with two-thirds (68%) of advised clients over 50. Just 14% of those in their 40s use advice, and just 4% under 30 do so.

There is evidence that this demographic is more disengaged with their finances. Royal London’s advice gap research found that 44% of 18 to 34-year-olds have little awareness of their own financial situation and seeking advice isn’t something they’ve thought about[iii]. However, developing a proper financial plan early in life has never been more important. Several trends threaten younger generations financial health, such as longer life expectancy, defined benefit pensions are shifting to defined contribution, and the fact that younger generations are less often homeowners.

We need to engage younger people with advice as the clients of the future, for their own benefit and to safeguard the long-term health of the sector.

Relationship differences

Surprisingly, our analysis suggests that relationship status could be the biggest indicator of your likelihood to get advice. Nearly half (44%) of advised clients in our dataset are married or in a civil partnership, compared with just 11% who are single, 6% widowed and 1% divorced.

There could be several factors at play here. Older people are more likely to be married – according to the Office for National Statistics (ONS), five times (19%) as many people aged 70 years and over are married than those under 30 years (3.7%)[iv] – and, as mentioned earlier, older people are also more likely to take advice. In addition, a marriage commitment often coincides with other life events, such as having children and buying a house, which can prompt people to take advice.

The ONS data shows that marriage rates are falling and cohabiting increasing, so it will be interesting to see whether our data on the relationship status of those taking advice will change over time.

Geographic variations

Our data also highlights that where you live plays a role in whether you take advice. Scotland and the South West of England have the greatest proportion of the local population receiving advice, each at 7%, while London and North East England have the least, at 4%.

There’s a perception that people don’t take advice because they don’t have enough money. While this is likely true to an extent, our geographic data suggests that it’s not quite that straightforward.

The North East is the second poorest region in the UK (after Northern Ireland), with a gross disposable household income (GDHI) per head of £17,663 according to the Office for National Statistics[v]. This may account for fewer people there taking professional advice. However, London is the richest region with £31,094 GDHI per head, and the take-up of advice there is also very low.

Possibly the capital’s position as a centre for financial services means more wealthy people in London choose to manage their own finances. Or it might be the fact that London’s population has a median age of 35.9, compared to 44.1 for those in the South West of England according to ONS figures[vi], and as we’ve seen younger people are less likely to take advice. It’s easy to speculate, but it seems that taking advice isn’t just about having the most disposable income.

Widening access to advice – good for clients and advisers

The Advice Map of Britain shows that married men over 50 are prevalent among advised clients, accounting for one in five individuals receiving financial advice . Finding ways to engage more women, younger generations and single people with their long-term finances and reduce geographical disparities is crucial to widening access to advice.

As well as the positive impact on society and people’s futures, there are major business benefits to addressing the advice gap too. According to the Royal London advice gap research, around 39 million adults in the UK fall into the advice gap, but of those 3.7 million people are open to receiving professional financial advice and have investible assets worth over £50,000, creating a £185 billion opportunity for advisers.

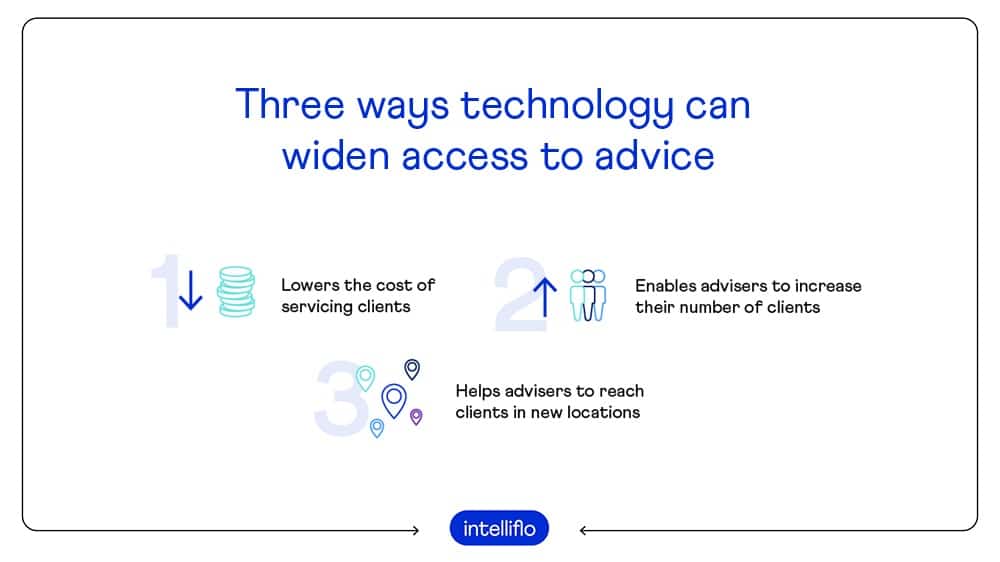

Technology’s threefold impact

Embedding technology within the advice journey is key to opening up advice to new audiences and delivering significant benefits to clients, while at the same time ensuring continued profitability.

By streamlining adviser processes, technology can improve efficiency and overall business performance and lowers the cost of servicing clients. Our 2022 e-Adviser Index, which analyses a firm’s business metrics alongside its use of intelliflo office, reveals that advisers who use all parts of the system generated 54% more revenue per adviser and 76% more ongoing revenue than firms using just the core functionality.

Technology can also improve a firm’s capacity to manage more clients with the eAdviser Index showing that high-tech adopters can service 39% more clients than their low-tech counterparts. With the low growth in adviser numbers we’ve seen in recent years, helping firms manage more clients without increasing headcount will be central to broadening access to financial advice.

In addition, technology is vital in supporting advisers in widening the reach of their firm into new geographical locations as well as servicing clients who prefer to access information outside of normal working hours. By using client portals and virtual meetings, advisers can meet the needs of today’s hectic lifestyles, or expand beyond their traditional radius for in-person meetings to offer advice regardless of the client’s location.

With persistent inflation, high interest rates, economic uncertainty and volatile markets, many people now face serious financial challenges, making financial planning more important than ever. Advisers remain crucial to delivering quality financial planning, but technology holds the key to bridging the advice gap and supporting firms’ long-term success.

[i] Advice Tech Foundations, NextWealth, September 2023

[ii] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1081397/Individual_Savings_Accounts_ISAs_Tables_June_2022.ods

[iii] https://adviser.royallondon.com/articles-and-guides/research/advice-gap/

[iv] https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/bulletins/populationestimatesbymaritalstatusandlivingarrangements/2020

[v] https://www.ons.gov.uk/economy/regionalaccounts/grossdisposablehouseholdincome/bulletins/regionalgrossdisposablehouseholdincomegdhi/1997to2021

[vi] https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/datasets/populationestimatesforukenglandandwalesscotlandandnorthernireland