Best ways to boost client engagement in challenging times

Nick Eatock, CEO of intelliflo

The issue of inflation has gained significant attention over the last few years. But while prices are now rising more slowly, it doesn’t mean the cost-of-living crisis is over.

Advisers face the ongoing challenge of keeping clients engaged with their long-term financial plans, while managing the increasing day-to-day demands on their cash.

Inflation has fallen significantly from 11% in 2022 to 3.4% now, according to the latest data from the Office for National Statistics. Although it currently remains above the Bank of England’s 2% target, Office for Budget Responsibility (OBR) figures issued alongside the recent Budget estimate it will drop further, to 2.2% by the end of this year and 1.5% in 2025.

Despite these welcome falls, however, prices remain far higher than they were two years ago and many continue to rise, just more slowly. Research by Nationwide has found that, on average, household energy bills have increased by 63%, fuel by 39%, food by 32%, rent by 26% and mortgages by 22% since 2021.

Two-fifths (43%) of respondents to its survey said their financial situation is worse now than six months ago.

In addition, figures from the Resolution Foundation highlight that wages have risen more slowly than prices. It forecasts that real wages will be no higher this year than they were in 2006, impacting living standards at almost all income levels.

While OBR figures suggest the Bank of England base rate is set to fall from the current 5.25% to 4.2% by the end of 2024, and many commentators are suggesting the inflation figures may result in an earlier than expected rate cut, this may not be enough to insulate mortgagees from rate rises. The Resolution Foundation predicts 1.5 million households will have to re-mortgage this year, with average annual costs increasing by around £1,800.

As a result of rising costs, people are having to change their long-term financial plans. According to its interim results statement, Hargreaves Lansdown saw a year-on-year increase in outflows, mostly from its fund and share accounts, attributing the withdrawals to cost-of-living issues and clients transferring money to cash ISAs.

Even advised clients, who are often better prepared financially for unexpected events than direct investors, are withdrawing money from their investments at record levels.

Figures from the lang cat show outflows from advised platforms stood at £53.18bn for the year, up by more than a third on 2022’s total of £39.01bn. The consultancy said advisers attributed this in part to supporting themselves and family members with increased household expenses.

The ongoing issue of inflation and the Bank of England’s hikes to the base rate to dampen it are affecting an increasing number of people’s finances. More people are making difficult choices and, while typical advised clients may not be torn between heating and eating, they might be considering actions such as reducing regular investments or pension payments to manage rising mortgage costs.

A study by the Pensions Management Institute revealed more employees are changing their pension contributions due to cost-of-living concerns, with a quarter (23%) of respondents reducing them and one in 20 (5%) stopping them altogether.

For advisers, providing reassurance and keeping clients engaged with their financial plans in challenging times is a key part of the job. You can only support clients in making informed decisions if you are fully abreast of any changes in their financial situation.

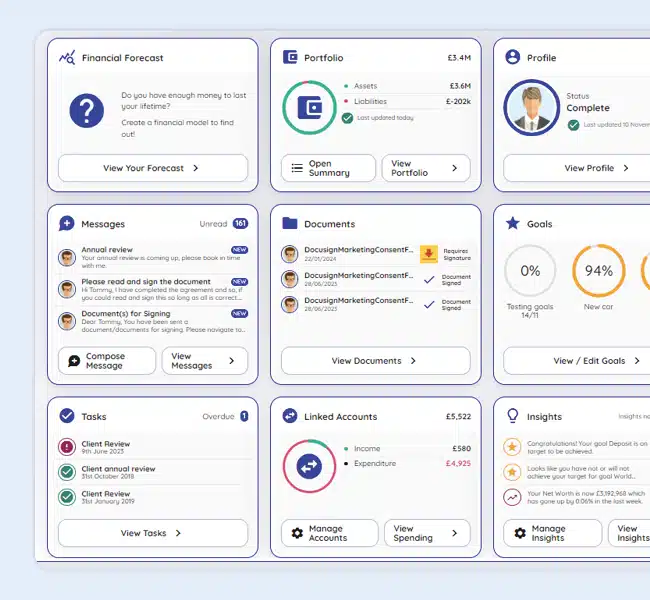

Technology has an important role to play in helping maintain communication and driving engagement. For instance, by allowing investors to securely access their financial data at any time and from any location or device, portals can be hugely beneficial to the advice process.

Offering a single view of the client’s advised financial products and non-advised products, including current account transactions, savings and debt if connected by open banking, provides a clear picture of their overall situation.

Using portals to securely share and sign documents electronically reduces friction in the advice process. Removing the need to wait for hard copies to be posted, signed and returned keeps things moving and helps ensure clients don’t disengage due to the inefficient admin sometimes associated with financial services.

Cashflow modelling tools can also bring a plan to life for the client and can support advisers in testing plans at the outset and on an ongoing basis, especially if any circumstances change. Putting a simplified version of these tools in the client’s hands via a portal can also support engagement with the advice journey. Clients can play around with different choices in their own time and get a better understanding of what’s possible, which they can develop further with their adviser.

Despite the falling inflation rates, for many people rising living costs remain an issue. Inflation should fall further this year and, with it, the Bank of England base rate, but the disparity between rising prices and real wages continues to put a strain on household finances.

Using technology throughout the advice journey can help firms stay up to date with clients’ changing circumstances and plan flexible solutions as their needs evolve, ensuring clients remain engaged with their finances and on track to meet their future goals.

This article was first published in moneymarketing on 19th April. Please find a link to the original piece here.

Please find more information on intelliflo’s client portal here.