Is your client data helping or hindering clients’ engagement with your firm?

Richard Wake, Chief Customer Officer, UK and AUS

With today’s 24/7, on-demand technology, clients are increasingly seeking more frequent interaction with their finances digitally, alongside face-to-face contact with their adviser at an annual meeting. By embracing this switch to digital, and using technology to exploit client data, firms can improve the client experience and drive business growth.

Meeting digital expectations

Although the trend towards digital started long before this decade, the movement restrictions of the early 2020s led to people becoming very comfortable interacting online, including managing their finances. According to analysis by comparison platform finder.com, 86% of UK adults, some 46 million people, use a form of online or remote banking. This growing confidence around completing financial transactions online extends to wealth management too.

At intelliflo, the switch from in-person to digital enforced by the Covid19 restrictions saw the number of advised clients registered on our client portal surge by 300% during the pandemic. The high level of usage has continued since with one in 150 UK adults now using our client portal.

Over recent years, we’ve also seen both firms and clients engaging more frequently with intelliflo software, with huge increases in the number of secure messages sent and documents shared digitally as well as usage of the electronic signature tool DocuSign.

This switch to digital has also opened up new opportunities for firms to make better use of the data they hold on clients. Here we look at three ways financial advice firms can use technology to help make sure the data you hold benefits both your clients and your business. Keep in mind that ensuring clients have easy access to the latest accurate key information is essential under the Consumer Duty ‘customer understanding’ outcome.

1. Ensuring accurate data via a client portal

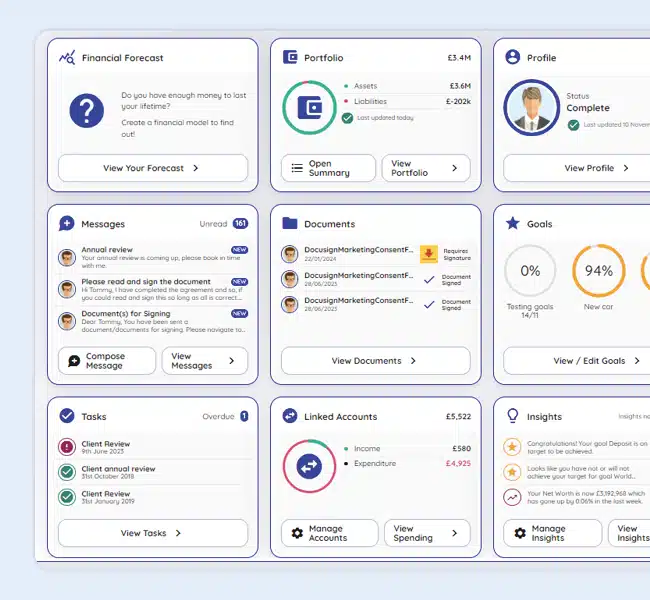

As well as giving clients the ability to see their portfolio valuation and relevant details, client portals can also help ensure the information you hold is correct by putting them in control of their personal data. This can support the initial fact-find and onboarding process and also speed up the data gathering process in advance of regular meetings.

Minimising errors will improve the efficiency of your advice process, and keeping accurate client records will also help you stay on the right side of the regulators as this is a UK data protection requirement.

Putting the client in charge can also encourage them to provide a more complete picture of their finances, including linking to their non-advised finances via Open Banking. Advisers uncovered £20m worth of held-away assets in just three weeks when intelliflo launched its Open Banking functionality in 2021, and clients continue to embrace the aggregated view of their finances.

Linking to clients’ other financial providers can also provide up-to-date banking and credit data to streamline mortgage applications, and gain an accurate view of clients’ incomings and outgoings to better inform cashflow projections.

2. Driving engagement through data visualisation

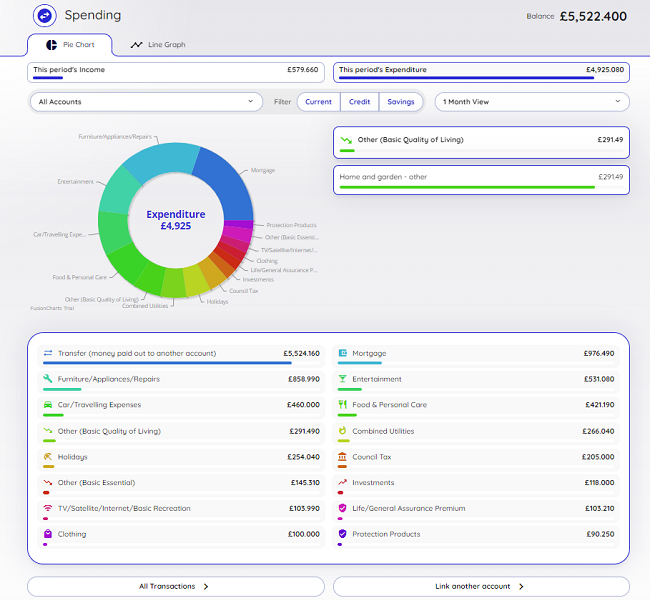

Helping your clients understand where their finances are and where they need to be to meet their financial goals is increasingly important in the financial advice process. Feeding client data into cashflow planning tools brings that data to life, helping you build, stress-test and adapt the financial plan while visually engaging your clients, via interactive charts and graphs.

Knowing that their finances are on track will foster greater confidence in the advice process, making sure clients stick to the plan. However, such tools are only as good as the data you put into them – having access to accurate information is crucial.

Creating an emotional connection between your client and the advice process through data visualisation can encourage greater engagement with the plan. Giving your clients a clear picture of their future finances also helps demonstrate the value of your advice, supporting the Consumer Duty focus on price and value.

According to 2023 research by Morningstar, consumers cite the emotional parts of the process, such as providing reassurance and guidance, and creating trust in the plan as the reason they take financial advice, rather than financial aspects like being on track for retirement or setting up specific products.

3. Keeping data secure

With data security a major concern for many people, providing your clients with a secure messaging functionality can offer peace of mind that you are taking your responsibilities around their information seriously. Secure messaging via a client portal enables you to store and share documents conveniently and safely, and allows clients to sign and return them electronically. This streamlines the advice process and reduces costs, removing the need to print and post paper documents.

Using secure messaging can also make sure you do not fall foul of the Information Commissioner’s Office (ICO). The ICO’s latest data shows that 248 reports of personal data breaches were received for the finance, insurance and credit sectors in Q2 2024.

While phishing caused the greatest number of problems, with 56 reports, the second most common breach in our sector was data being emailed to the incorrect subject, with 45 reports.

Even with the rise in digital communications, data being faxed or posted to the wrong person still accounted for 20 breaches during the quarter. Given that the ICO can impose fines of up to £17.5m or 4% of annual turnover for the most serious infringements, ensuring client data is handled securely is crucial.

How we can help

We now operate online in so many aspects of our lives, that clients increasingly expect the opportunity to interact digitally with their financial planning too. Of course, there is still an important place for face-to-face advice, but by using technology to make the most of your client data, you can deliver the best outcomes for both your business and your clients.

Get in touch for more information on making your client data work for you.

This article was first published in FT Adviser on 10 January. Please find a link to the original piece here.